November 6, 2025

The Advisor Gap

Why $30M–$300M Families Have Nowhere to Turn

By Adam Reinking, CFA, CFP®

Most people in your situation are forced to take a terrible job that they never asked for.

See if this sounds familiar:

You have a CPA who reaches out every February to file returns. Your estate attorney surfaces every couple years when something major changes. You have a handful of investment managers operating in complete silos. Your insurance broker pops up conveniently around renewal time. You have K-1s scattered all over the place, real estate ventures, positions in sub-entities of sub-entities…

A hundred balls in the air, each of which could cost you millions if dropped. And who’s the juggler?

You.

You didn’t go looking for this job. Nobody handed you a title and a desk. But over time, as the net worth climbed and the entities multiplied and the private investments stacked up, you became the de facto CFO of your own family’s wealth.

It’s on you to coordinate people. It’s on you to chase K-1s and filings. It’s on you to understand the disparate factors that affect each other.

It’s stressful. It’s time-consuming. And it’s a huge risk to your legacy.

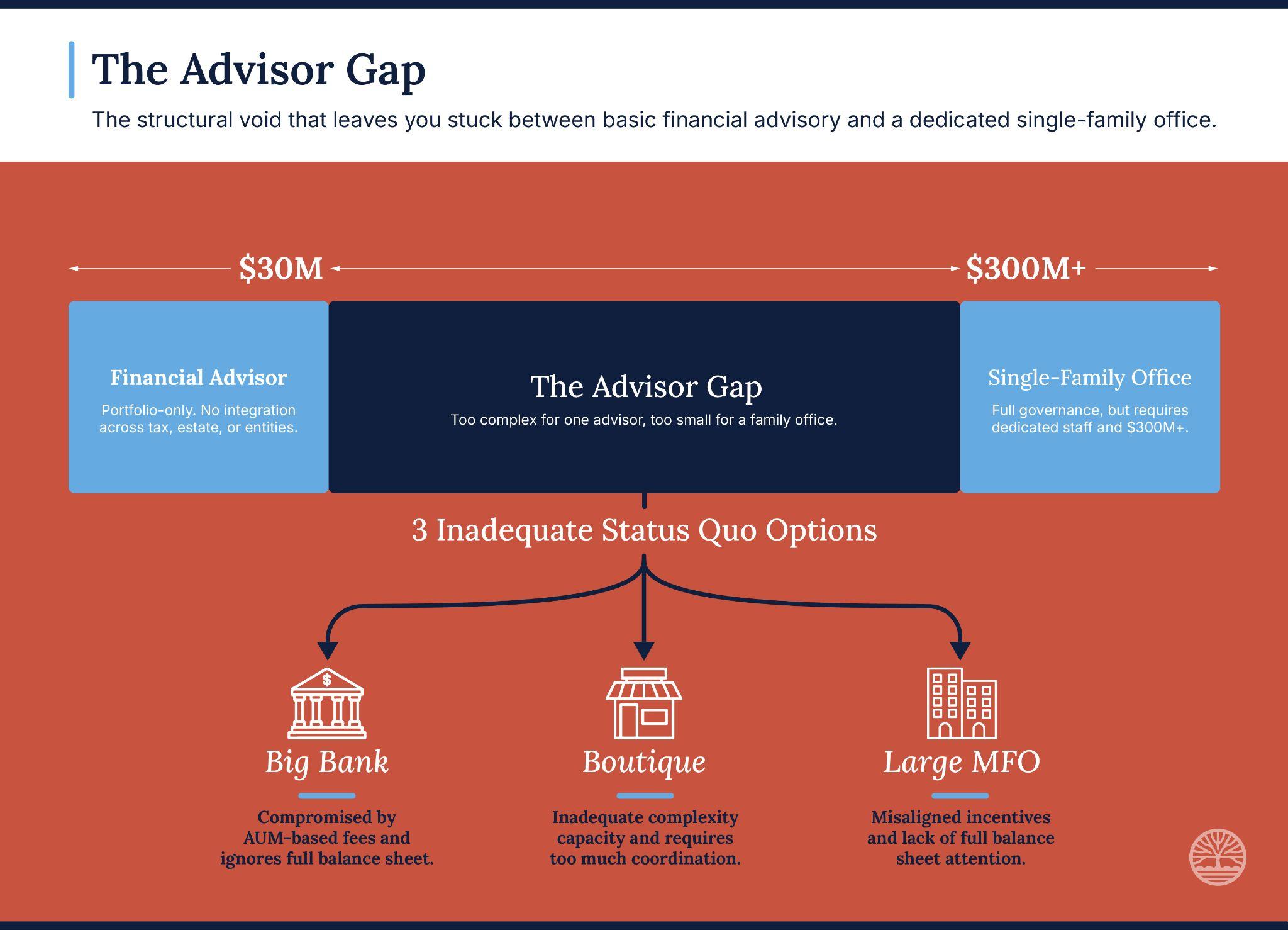

If any of this sounds familiar, you’re stuck in a place we call the Advisor Gap. And you’re not alone.

Why The Advisor Gap Exists

The wealth management industry is organized around two extremes. Below roughly $30 million net worth, competent RIAs and financial planners can serve you fairly well. They handle portfolios, basic planning, and straightforward tax coordination. The tools generally work and the economics typically make sense.

Above roughly $300 million, families can justify building a dedicated single-family office. Full-time staff. In-house tax and legal professionals. Custom reporting infrastructure. Deal sourcing capability. Payroll for this setup can be several million dollars per year. But at that asset level, the math works.

Between those thresholds sits a structural void. Families with $30 million to $300 million in net worth occupy a unique band of wealth management, and the industry has no native solution for them. They have operating businesses, private equity holdings, real estate across multiple entities, trusts with layered generational obligations, and tax situations that change materially from quarter to quarter. Their complexity resembles that of small institutions.

Their advisory options do not.

In our research, the majority of our clients identified this gap as the single most common frustration. The second most cited issue, the lack of integration across advisors, reinforced the reality of the gap. These are families who had either outgrown previous advisors, been disappointed by larger platforms, or were confronting the need for coordinated strategy for the first time.

The stark reality of the gap is that it’s built into the economics of the industry. And everyone who lands in it faces the same three inadequate options.

Three Status Quo Options, Same Dead End

The first option is the big bank or private bank. The prestige is real. The brand carries weight. But inside the relationship, the “relationship manager” is mandated to push products that generate revenue for the institution. Their profit relies on proprietary funds, lending spreads, and structured products with embedded fees. The advice is filtered through the bank’s profit model before it reaches the client. Investment management gets attention because it’s billable. The rest of the balance sheet, from private holdings to entities to tax architecture, gets acknowledged in the pitch, but neglected in practice. Your only hope of leverage is being the squeakiest gear in their client allocation. Once again, you’re stuck managing someone else just to make sure your interests are best served.

Worse yet?

You’ll never escape the inherent friction due to misaligned incentives. The banks are incentivized to push you into products that generate fee-based profits for them. If you have other priorities, that’s a problem for the bank. Here’s a perfect example:

We recently met with a $250M private equity operator who runs his own investments and has built a business investing other people’s capital alongside his own. His personal and professional finances are heavily intertwined. He has a team of people, including good accountants and finance professionals who can operate his books.

The banks can’t work for him because their revenue model doesn’t support his situation. His wealth is concentrated in his PE fund, SaaS-related holdings, and private investments. There’s very little sitting in liquid, publicly traded assets for a bank to manage and bill against. The AUM model generates no meaningful revenue from a client like this because the billable slice of his balance sheet is a fraction of his actual net worth. He’d just paid down a $45 million line of credit, which tells you where his cash flow goes: it cycles through the businesses and private positions, not into a managed portfolio.

His staff could handle the transactional side: accounting, books, financial reporting. What nobody was doing was looking at the overarching picture on income tax, estate tax, and cash flow across the full landscape. He had resources addressing pieces, but he never found a relationship that pulled it all together.

Once we had a look at this financial landscape?

We identified a couple million dollars a year in tax savings in the proposal. No one else had any strategies to serve his exact situation and identify such a massive immediate ROI. His response was “this is the first thing we have ever looked at that will actually work.” It’s a classic response we hear often from UHNW individuals stuck trying to hire banks to help them escape the Advisor Gap.

So, What About the Alternatives to Big Banks?

The next option is the local boutique. They’re smaller firms with more personal relationships and often better intentions. Unfortunately, most boutiques are still running asset-based fee models, which means the structural conflict around incentives remains. And functionally, few have the infrastructure to serve a $50 million multi-entity balance sheet at the level of sophistication it demands.

The lack of infrastructure and specific expertise means you find yourself stuck with fragmented tools and manual workarounds, which means you spend as much time managing the boutique as the boutique spends managing your wealth.

This leads many people in your position to explore the final option:

The large multi-family office. This is supposed to be the answer. Institutional capability with white-glove service. In practice, clients end up experiencing the worst of both the big banks and the small boutiques. First, these large MFOs subscribe to the standard industry practice of an AUM-based fee model. This automatically disqualifies them from being the best stewards of complex wealth. Second, they’re big enough to structurally experience the same lack of client attention that also plagues the big banks. Teams rotate. Structures reorganize. Clients who signed up for intimacy and continuity find themselves feeling “handled” by a revolving cast of junior associates. Not only does this make for a crappy experience as a client spending substantial money, the discontinuity also carries inherent risk. In a world where one missed document could result in millions of lost opportunity costs, that’s a very real threat.

It’s the classic case of organizations trying to get the best of both worlds while the client ends up experiencing the worst of both worlds.

Given these three insufficient approaches, it’s no wonder so many UHNW individuals are stuck feeling like they have to compromise on at least one non-negotiable.

We see this pattern play out with venture operators, physicians, founders, and executives who built significant wealth through concentrated positions and complex business structures. The specifics change, but the theme is always the same. They’ve assembled advisors and professionals who can address pieces of their financial picture, but they’ve never found a true decision partner to help them bridge the Advisor Gap:

Someone that can look at everything, pull it together, and make sure the family is being well taken care of.

It taxes their time. It taxes their energy. And it most certainly taxes their wealth.

The True Costs of The Advisor Gap

So why do so many families tolerate this situation?

Because the cost of hiring someone is quantifiable. It’s a number on a proposal. The cost of doing nothing is invisible. Nobody sends you an invoice for the tax savings you missed because of the K-1 error your CPA overlooked, the entity restructuring that never happened, or the estate plan that’s three liquidity events out of date. You can’t calculate what you never knew you lost.

It’s a recipe for tolerating the simmer, sometimes for years.

Until the heat becomes unbearable. A tax bill that stings more than expected. Your spouse asks a question that nobody in your advisory constellation can answer: “What happens to all of this if something happens to you?” A pending liquidity event breaks the current skeleton crew model, and you’re left on an island to figure it out. Each of these moments adds weight. And eventually, the cost of inaction becomes visible enough to act on.

Our clients all reached the point where they began to clearly see the massive costs of the Advisor Gap.

When no one coordinates across tax, estate, and investment strategy, the most valuable planning opportunities go unexecuted. K-1 errors go uncaught because the CPA is filing hundreds of returns and doesn’t have bandwidth to read every document line by line. We routinely catch mistakes that swing tax bills by six figures. In one recent case, a single missed expense on one K-1 out of a hundred resulted in a $300,000 correction in the client’s favor. That error had been sitting there, invisible, waiting for someone to actually read the document.

Capital calls get missed because nobody is tracking the commitments. Investment sponsors send distributions to the wrong account, and without active reconciliation, the client would never notice. These aren’t rare events. They happen routinely when no professional system sits at the intersection of a complex financial landscape.

Then there’s the structural cost that compounds year after year. Estate plans that haven’t been updated since the last liquidity event. Asset location decisions made without tax consequences in mind. Entity structures that were built for a previous chapter of the family’s wealth and never redesigned for the current one. Each of these represents real dollars left on the table, compounding in the wrong direction. And because no one is measuring it, no one feels the urgency to fix it.

Finally, there’s the need for wise wealth stewardship. As complexity grows over time, so does the fragility of the entire system when it relies on you to hold all the pieces together.

One client came to us with 17 separate bank accounts, each holding $250,000 for FDIC coverage. He’s 75. He told us his wife wouldn’t be able to find all of them if he died. Until he talked to us, he didn’t know that single-account FDIC solutions existed. The complexity he had built over decades was functional for him, but it was fragile. This risked leaving his wife one event away from inheriting an operational crisis on top of a massive life-changing event if he passed away.

That’s just one of many hidden dangers of The Advisor Gap. The cost isn’t always dollars. It’s often the risk that everything you’ve built becomes unmanageable the moment you’re no longer the one managing it.

What the Bridge Looks Like

For families stuck in the Advisor Gap, the question worth asking is what a genuine solution would require. The criteria are specific.

-

It would need to integrate tax strategy, estate planning, and investment management under one coordinated team, with real-time visibility across the full balance sheet, including private and illiquid holdings.

-

It would need a fee structure that aligns the advisory team’s revenue with the actual work being done, tied to the complexity of the engagement rather than the size of the portfolio, so the entire wealth landscape receives attention regardless of liquidity.

-

It would need to be proactive and strategic, using reporting to architect what should happen next rather than simply showing what happened last quarter.

-

It would need a senior team that knows the family deeply and remains stable over time, with institutional-grade reporting infrastructure underneath so the system survives any individual person.

-

And it would need to absorb the coordination burden entirely, so the client stops acting as the unpaid project manager of their own wealth.

These are solvable problems. The industry simply hasn’t organized itself to solve them for the $30 million to $300 million band, because they can’t figure out the economics, and the complexity demands a different operating model than what they’re built to deliver.

The structural Advisor Gap in the market is clear, and we founded Redbud Advisors to fill it. Our mission is to remove the burden from the families stuck in this gap so they can pursue what matters most without sacrificing their means to do so.

If you’ve felt the weight of carrying this burden yourself, or ever wondered if the unknowns are eating away at your wealth, those are your cues to have a conversation with us. In just the first meeting, we typically discover unpulled levers that can save you substantially in taxes. And that’s just the start. You don’t have to prepare anything. Just reach out, and we’ll take care of the rest.

— Adam